In September of 2022, I had pneumonia. I didn’t know that at the time and went to a local CVS to get a COVID test. While I was in the treatment room, I collapsed, and an ambulance was called to take me to the hospital.

A year later, I got a bill from the ambulance company. I called my insurance and was told the bill had been paid. I would often get “non-bills” from my insurance—those explanations of benefits that show what was charged, what was paid, and what might be left. I figured this was just another one of those.

In 2024, I was at work and started getting calls from a debt collector.

Yes. They called my work.

I spoke to a man who informed me I had been sent to collections for not paying a $1,400+ balance from that ambulance ride.

This time, I checked my insurance online. It clearly stated 100% coverage for ambulance services, both in-network and out-of-network. Once I had that information in front of me, I called my insurance company to find out what was going on.

Want to know what I was told?

“Yes, you have 100% coverage, but that doesn’t always mean 100% is paid.”

Uh… what???

I got HR involved, and within days, I had a check mailed to me that I then had to forward to the debt collector.

Fast forward to 2025.

I was away from home and thought I had the stomach flu—until I began hemorrhaging. I was so weak I didn’t feel safe driving. Most of my family in the area was at work or unable to help, so I called an ambulance to take me 1.5 miles to the hospital.

Six months later… another debt collector.

I had received something in the mail from the local ambulance company, but it looked exactly like the donation letters my mom gets all the time. I was wrong in assuming that was all it was.

This time, I owe $886 after my insurance paid $588.

That is a very expensive 1.5-mile trip.

This time, my insurance gave me a little more information—and I’m passing it along.

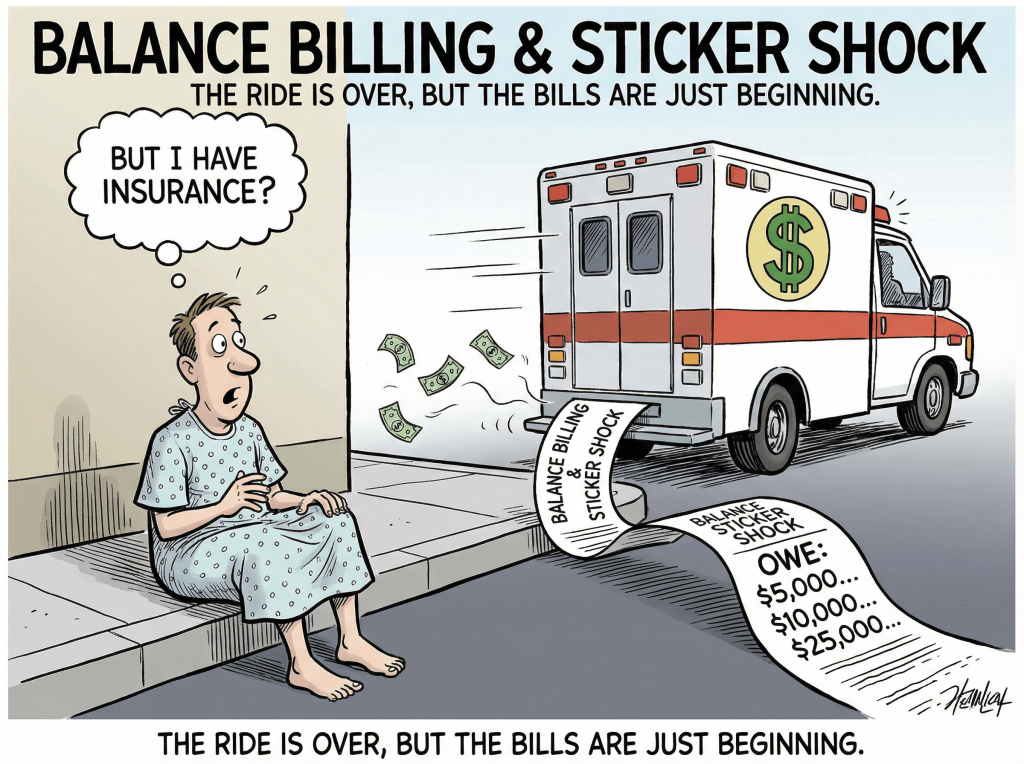

Balance billing is very common in the ambulance world.

When I questioned that with insurance, I was told:

“Ambulance overcharging is out of control.”

I can’t say whether I agree or disagree, although the only treatment I received in the vehicle was having my vitals checked and giving a history. I don’t think that was worth almost $1,400, but I digress.

A key issue I learned:

Most ground ambulances are considered out-of-network, because they contract with multiple systems. So if your insurance only covers in-network services, that’s a red flag.

I also learned about the Federal “NO SUPRISES ACT”.

According to the Centers for Medicare and Medicaid Services, the federal No Surprises Act, effective January 1, 2022, protects patients from most surprise billing for:

- Emergency services

- Out-of-network providers at in-network facilities

- Air ambulance services

It limits patient cost-sharing to in-network levels and applies to most employer-sponsored, marketplace, and individual health plans.

The U.S. Department of Labor further explains key takeaways of the Act:

- Emergency Care: You can’t be billed more than in-network rates for emergency services

- Out-of-Network at In-Network Facilities: You’re protected from surprise bills (like anesthesiologists)

- Air Ambulances: Covered under the law

- Consent Exception: You may waive protections in limited cases

- Good Faith Estimates: Uninsured/self-pay patients can request cost estimates

What is NOT covered:

Ground ambulances.

Yes. Really.

Why, you ask?

That’s a good question.

The No Surprises Act leaves out ground ambulances—and honestly, it’s not because they don’t matter. It comes down to how complicated the system is. Ambulance services aren’t one-size-fits-all. Some are publicly funded, others are private, and many operate within messy local funding structures that don’t translate neatly into federal policy. On top of that, there isn’t consistent cost data across the board.

Lawmakers were concerned that if they rushed in and capped payments without fully understanding the system, they could unintentionally push some local ambulance services into financial collapse. And if those services disappear, that’s not just a billing issue—it’s an access-to-care issue.

So for now, ground ambulances were left out while more data is being collected.

Not ideal. But very much a “we don’t want to break the system while trying to fix it” situation.

What does this mean?

It means we are still open to balance billing—and debt collectors.

And here’s the reality:

You don’t exactly shop around when you need an ambulance.

Balance billing—simple version:

When you take an ambulance, the service bills your insurance. Your insurance pays what they consider “reasonable” or “allowed.” If the ambulance provider charges more than that—and they often do—the remaining balance gets billed to you.

That leftover amount?

That’s balance billing.

Example:

- Ambulance charges: $2,000

- Insurance allows: $800

- Insurance pays: $600

- You owe: your copay + $1,200

And unlike many other emergency services, ground ambulances are not fully protected under the No Surprises Act—so they can legally bill you for that difference.

Why this hits so hard:

- You don’t get to choose your ambulance provider

- Most ambulance services are out-of-network

- Costs vary wildly

- It happens in true emergencies—when you have zero control

So people end up with large, unexpected bills after what was already a stressful—or life-threatening—situation.

There are ongoing efforts to fix this, but right now, it remains a major gap in patient protection—one many people don’t realize exists until they’re staring at the bill.

Approximately 22 states have some form of protection, but they vary widely and often:

- Only apply to emergency transport

- Only apply to certain insurance plans

- Exclude some ambulance types

- Don’t apply to self-funded employer plans

Which means millions of people still have little to no protection from these bills.

I’m lucky. I was able—again—to get my insurance to cover the balance.

Because the reality is… I couldn’t afford it.

Not now. Not while I’ve been on long-term disability since that fated ambulance trip.

So what now? I’m reaching out to my federal and state officials—because no one should be dealing with this on top of a medical emergency.

Bottom line:

Ambulances should get paid a reasonable amount for their critical work in the field, but not at the expense of people in crisis. Balance billing is major gap in the system. One that hits people when they’re already at their worst.

And now?

It’s not just about paying the bill—it’s about pushing for change so no one else has to deal with this on top of a medical crisis.

I will keep you posted.

Leave a comment